Diving Into ARK's Genomic Revolution Thesis with AquaBounty ($AQB)

$ARKG owns 20%+ of the company's outstanding shares

In these volatile markets, I have been recently paying attention to what is going on at ARK Funds' actively managed exchange-traded funds. ARK Funds’ Genomic Revolution Multi-Sector actively managed ETF (ARKG) owns almost 9 million shares of AquaBounty Technologies (AQB). This represents ~20% of the company's outstanding shares. With a position size worth well over $100 million, ARKG’s position in $600 market capitalization company AquaBounty merits a closer look.

Company At a Glance

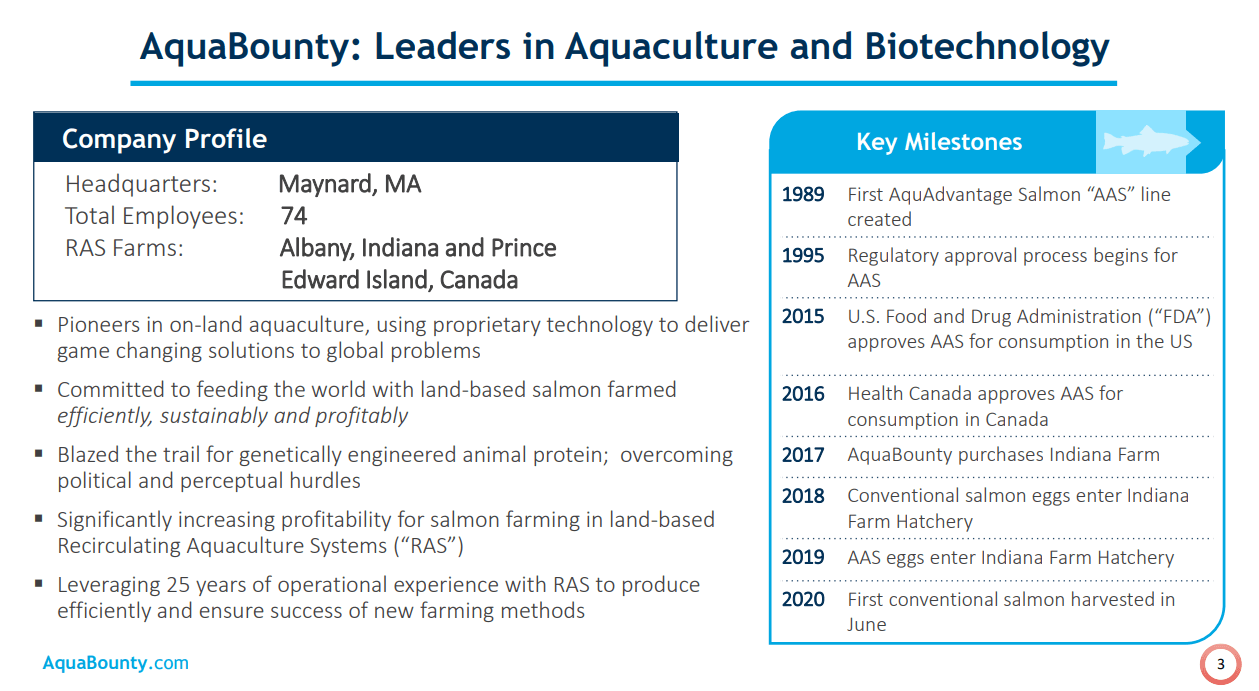

AQB was founded in the early 1990s and is headquartered in Massachusetts. Originally an aquaculture company, the company now is focused on products to enhance productivity and land-based aquaculture. It sells AquAdvantage salmon, a bioengineered Atlantic salmon for human consumption. As such, the company story plays directly into ARK’s Genomic Revolution thesis.

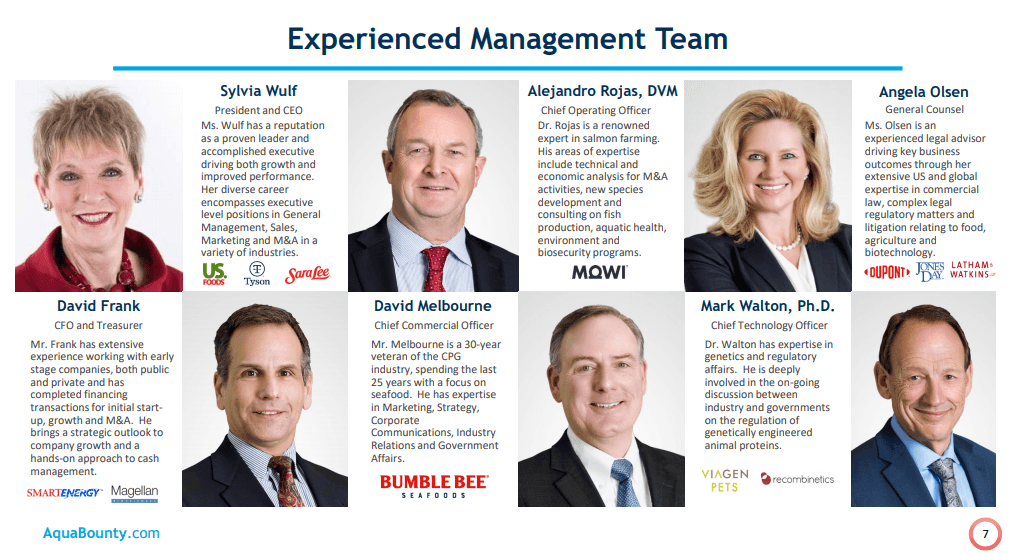

The company's management team has a diverse background with significant industry experience in seafood, genetics, and salmon farming. In addition, CFO David Frank has a strong background in growth capital and M&A, which should enable the company to simplify its finances and focus on capital-light expansion into the coming years.

Insider Buying and Financial Strength

There has been significant insider buying of AQB from board directors and large shareholders over the last months. Most recently, board director Richard Huber bought 10,000 shares on December 14th in the open market at an average cost of $6.50. AQB equity shares have been on a tremendous run over the past year. The company's equity shares have delivered multi-bagger returns to investors of late. With outstanding shares at ~45.4 million total, I believe this company could be well-positioned to continue to deliver shareholder value over calendar year 2021 as well. Notably, insiders and significant shareholders own over 40% of the company.

Of course, as the company share price has skyrocketed, management is taking advantage, by issuing secondary offerings into the significant investor demand in the marketplace. In December, the company closed a public offering of over $65 million, strengthening the balance sheet even further. Only days earlier, they announced that they were seeking to raise $57 million dollars, but given the significant oversubscription in the market, it was prudent to take advantage.

The company is building its Farm 3, and expects to begin construction this year, anticipating the location will be ready to commence commercial production in 2023. It's good that AQB raised capital recently, as they expect the total bill cost for Farm 3 to be over $140 million. Even with this expected capital expenditure taking place over the coming years, the company currently has a healthy balance sheet.

AquaBounty's Commercial Prospects

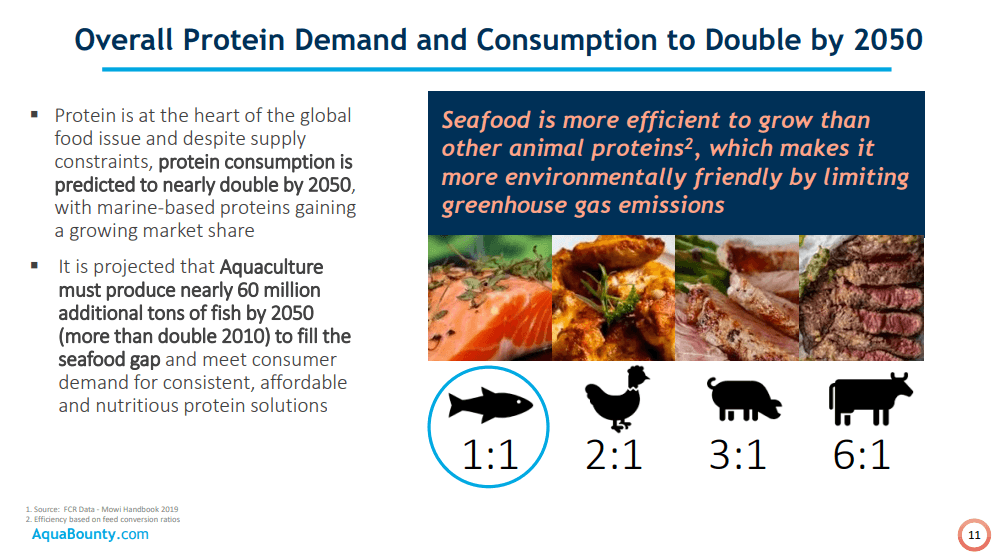

Let’s examine the commercial opportunity more carefully. The global salmon market is a huge market of over $17 billion. The company is well-positioned to capitalize on a massive supply-demand imbalance as the global population grows and middle-class incomes rise, which will have the effect of increasing aggregate demand for salmon. The company's AquAdvantage salmon has superior unit economics to conventional salmon and should allow AQB to maintain EBITDA margins twice as high as land-based farms that are raising conventional salmon.

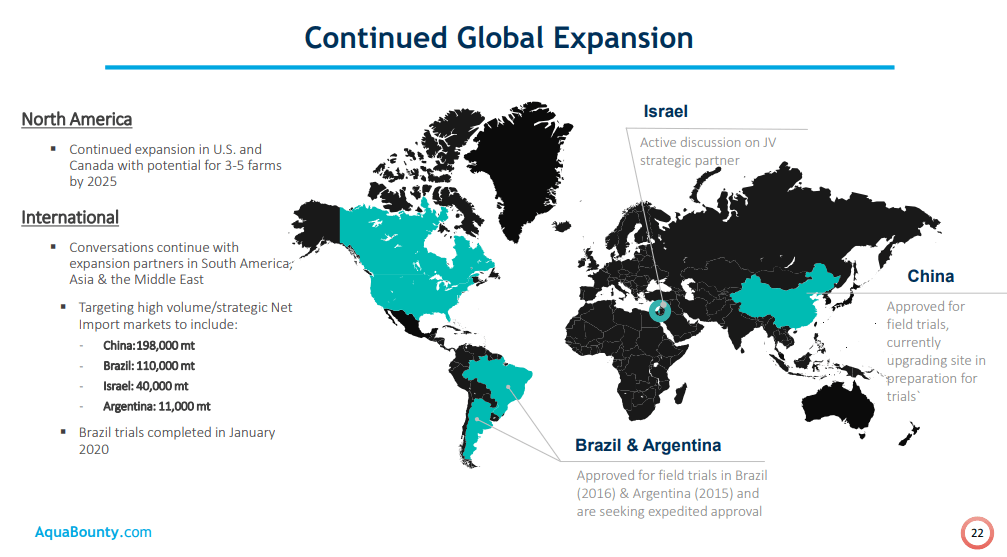

The company has a very interesting mission in a world where overfishing of various environments has been identified as a major problem. There should be an effective technological approach to serving the market demand for salmon. While there are other competitors seeking to make genetic progress in technology to disrupt the industry of land-based salmon farming, AquaBounty is the largest and best capitalized player in the space. Current valuations do project quite a bit of optimism for the company's progress; however, there will be significant de-risking over the coming two years as Farm 3 is turned online and the company continues to identify opportunities for global expansion with strategic joint venture partners across Israel, China, Brazil, Argentina, and other locations.

Risks

Risks to execution will include too much distraction across this global expansion and potentially higher than anticipated costs as the company seeks to increase its annual output capacity to justify an appropriate payback to equity investors.

I expect the company to be operating at net losses for the foreseeable future, but production output should significantly start to scale starting in 2023 once Farm 3 comes online and additional farms are able to be brought on in a non-dilutive way to equity. However, I would like to see a payback time horizon of shorter than the 7-8 years for Farm 3 which the company currently projects.

Conclusion

If AQB is able to execute on a business plan for growth, its market capitalization should be at least several billions of dollars. At this point, I would expect the company to be acquired or otherwise merge into a larger seafood company before the end of the current decade. There is significant work ahead for the management team at AQB, but there is also a lot of reason to believe that their gene-editing technology and different approach to land-based aquaculture should allow them to achieve very impressive results. Investors would be well-positioned to watch AquaBounty closely in the coming years. Good luck!